Insurance Claim Settlement Process USA:

Understanding the Insurance Claim Settlement Process in the USA

The insurance claim settlement process USA is a structured legal and financial procedure through which policyholders receive compensation after a loss, accident, or damage. Whether it’s auto insurance, health insurance, or property insurance, the process follows a similar pattern—but the payout amount and timeline can vary significantly.

Insurance companies are profit-driven, which means they often try to minimize payouts. That’s why understanding the insurance claim settlement process USA step-by-step is crucial if you want to maximize your compensation.

Types of Insurance Claims in the USA

Different types of claims follow slightly different procedures:

Auto Insurance Claims

- Car accidents

- Vehicle damage

- Liability claims

Health Insurance Claims

- Hospital bills

- Medical treatments

- Surgeries

Property Insurance Claims

- Home damage

- Fire or flood loss

- Theft claims

Life Insurance Claims

- Death benefits

- Term insurance payouts

Each of these categories affects how the settlement amount is calculated.

Step-by-Step Insurance Claim Settlement Process

Step 1: Incident Occurs

The process begins when an event happens—such as a car accident, medical emergency, or property damage.

Step 2: Notify the Insurance Company

You must inform your insurer immediately. Most companies require reporting within 24–72 hours.

Step 3: File the Claim

You submit a formal claim along with supporting documents:

- Policy details

- FIR (if required)

- Medical bills or repair estimates

Step 4: Claim Investigation

The insurance company assigns an adjuster who:

- Reviews documents

- Inspects damage

- Verifies claim authenticity

Step 5: Damage Assessment

The insurer calculates the compensation based on:

- Policy coverage

- Deductibles

- Depreciation

Step 6: Settlement Offer

The company provides a settlement offer based on its evaluation.

Step 7: Negotiation & Final Settlement

You can accept or negotiate the offer before final payout.

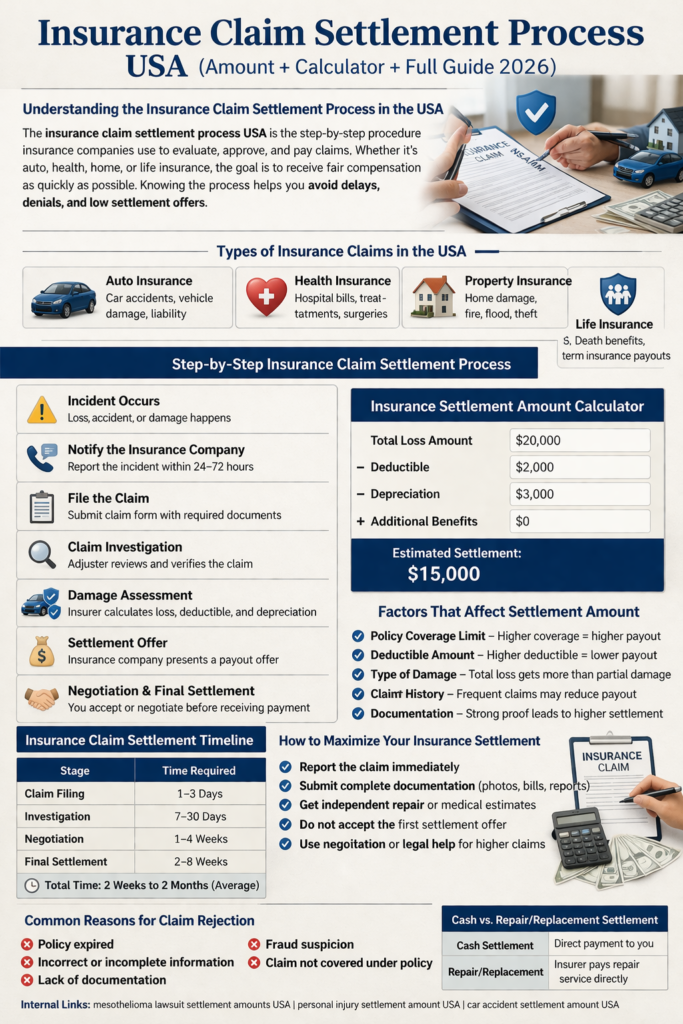

Insurance Settlement Amount Calculation

The insurance claim settlement amount USA depends on multiple variables.

Basic Formula:

Settlement Amount = (Total Loss – Deductible – Depreciation)

Example:

- Total Damage: $20,000

- Deductible: $2,000

- Depreciation: $3,000

Final Settlement = $15,000

Factors That Affect Insurance Claim Settlement Amount

Policy Coverage Limit

Higher coverage = higher payout potential

Deductible Amount

Higher deductible = lower payout

Type of Damage

Total loss gets higher compensation than partial damage

Claim History

Frequent claims may reduce payout

Documentation Quality

Strong evidence leads to higher settlement

Insurance Claim Settlement Timeline in the USA

| Stage | Time Required |

|---|---|

| Claim Filing | 1–3 Days |

| Investigation | 7–30 Days |

| Negotiation | 1–4 Weeks |

| Final Settlement | 2–8 Weeks |

👉 Total Time: 2 weeks to 2 months (average)

Types of Insurance Settlements

Cash Settlement

You receive direct payment

Repair/Replacement Settlement

Insurance company pays repair service directly

Structured Settlement

Payments are made over time

Common Reasons for Claim Rejection

Understanding this helps avoid delays:

- Policy expired

- Incorrect information

- Lack of documentation

- Fraud suspicion

- Claim outside coverage

How to Maximize Your Insurance Settlement

To get the highest payout:

- Report the claim immediately

- Submit complete documentation

- Take photos/videos as proof

- Don’t accept the first offer

- Consider hiring a claim attorney

👉 These steps can increase your settlement by 20%–50%

Insurance Adjuster Role (Very Important)

An adjuster is assigned by the insurance company to evaluate your claim.

Their Job:

- Inspect damages

- Verify claim details

- Estimate payout

👉 Important Tip:

Adjusters work for the insurer—not for you—so always double-check their assessment.

Settlement vs Claim Dispute (Comparison)

| Factor | Settlement | Dispute |

|---|---|---|

| Time | Fast | Slow |

| Risk | Low | Medium |

| Compensation | Moderate | Higher possible |

| Effort | Low | High |

Advanced Strategy to Increase Claim Value

- Get independent repair estimates

- Hire a public adjuster

- Use legal consultation

- Document emotional & financial losses

👉 These strategies significantly improve insurance claim settlement amounts USA

Early Settlement vs Negotiated Settlement

| Type | Benefit | Drawback |

|---|---|---|

| Early Settlement | Fast payout | Lower amount |

| Negotiated Settlement | Higher compensation | Takes time |

Real Case Examples: How Insurance Settlements Work in the USA