The Hidden Truth About Insurance Settlement for Car Accident USA

Imagine this…

You’re driving home after a long day. Suddenly — BAM!

A crash changes everything.

Within seconds, your life flips:

- Medical bills start piling up

- Insurance companies begin calling

- You’re confused, stressed, and unsure what to do

And the biggest question hits you:

👉 “How much settlement can I get?”

Here’s the reality most people don’t know:

Insurance companies are NOT your friends — they are trained to pay you the lowest possible amount.

This guide will expose:

- How settlements actually work

- How much you can claim

- Tricks insurers use to reduce payouts

- And how to maximize your compensation

What is an Insurance Settlement for a Car Accident?

An insurance settlement is the amount of money paid to you after a car accident to cover your losses.

It includes compensation for:

| Category | What It Covers |

|---|---|

| Medical Expenses | Hospital bills, surgeries, medicines |

| Lost Wages | Income lost due to injury |

| Property Damage | Car repair or replacement |

| Pain & Suffering | Emotional distress, trauma |

| Future Costs | Ongoing treatment, therapy |

👉 In the USA, most cases settle out of court, meaning you don’t need a trial.

Real-Life Example

Let’s take an example:

John (California)

- Rear-ended at a signal

- Minor injuries initially

- Later diagnosed with spinal damage

What happened next?

- Insurance offered: $8,000

- Actual settlement after lawyer: $85,000

👉 That’s a 10X increase

Why?

Because he understood:

- His rights

- Long-term medical impact

- Negotiation strategy

Types of Car Accident Insurance Settlements in the USA

1. Bodily Injury Settlement

This is the most important claim type.

Covers:

- Medical bills

- Rehabilitation

- Emotional distress

👉 Example: Whiplash, fractures, head injuries

2. Property Damage Settlement

Covers:

- Car repair costs

- Total loss value

- Rental vehicle

3. Pain and Suffering Settlement

This is where big money lies 💰

Includes:

- Mental trauma

- Anxiety, PTSD

- Loss of enjoyment of life

👉 Often calculated using multiplier method (1.5x–5x medical bills)

4. Wrongful Death Settlement

If a loved one dies in an accident:

Compensation includes:

- Funeral expenses

- Loss of income

- Emotional damages

👉 These cases can reach millions of dollars

Average Car Accident Settlement Amounts in the USA (2026 Data)

Here’s what people actually receive:

| Injury Type | Average Settlement |

|---|---|

| Minor injuries | $3,000 – $15,000 |

| Moderate injuries | $15,000 – $75,000 |

| Severe injuries | $75,000 – $500,000+ |

| Permanent disability | $500,000 – $2M+ |

| Wrongful death | $1M – $10M+ |

⚠️ Important:

Every case is different — your settlement depends on multiple factors.

Key Factors That Affect Your Settlement Amount

1. Severity of Injury

👉 More serious injury = higher payout

- Soft tissue injury → Low settlement

- Brain injury → Very high settlement

2. Medical Expenses

Insurance companies use this as a base calculation

👉 Example:

- Medical bills: $20,000

- Settlement: $40,000–$100,000

3. Fault (Liability)

Who caused the accident?

- 100% other driver → Full compensation

- Shared fault → Reduced payout

4. Insurance Policy Limits

Even if your case is worth $500,000…

👉 If the driver only has $100,000 coverage, you may get limited payout

5. Evidence Strength

Strong evidence = stronger case

Includes:

- Police reports

- CCTV footage

- Witness statements

- Medical records

How Insurance Companies Calculate Settlement

There is no fixed formula — but they use:

👉 Multiplier Method

Settlement = Medical Bills × Multiplier (1.5 to 5)

Example:

- Bills: $10,000

- Multiplier: 3

👉 Settlement = $30,000

👉 Per Diem Method

You get paid per day of suffering

Example:

- $100/day × 200 days = $20,000

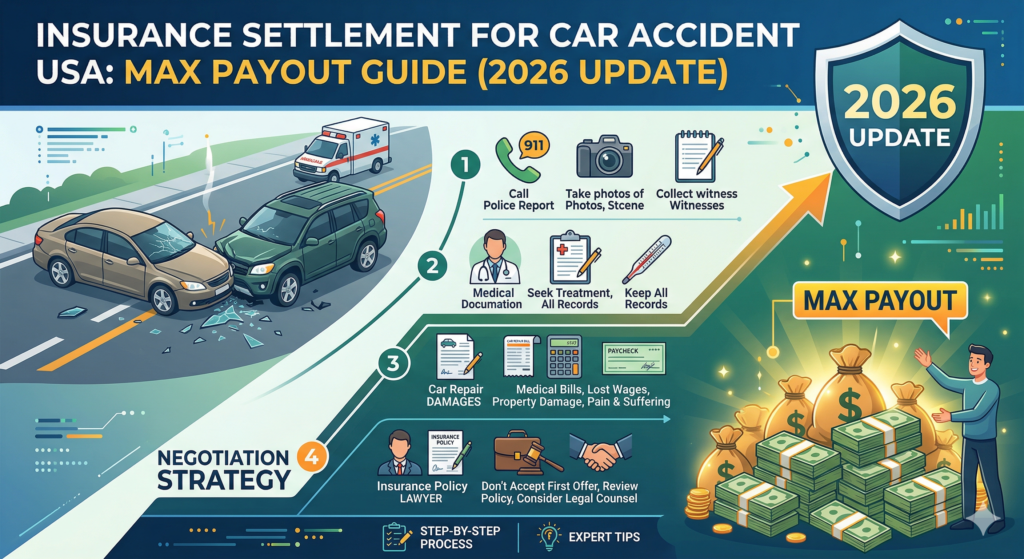

Step-by-Step Settlement Process (USA)

Step 1: Accident Happens

- Call police

- Get medical help

- Collect evidence

Step 2: File Insurance Claim

You notify:

- Your insurer

- Other driver’s insurer

Step 3: Investigation

Insurance company checks:

- Fault

- Damages

- Medical reports

Step 4: Settlement Offer

👉 First offer is usually LOW (very low)

Step 5: Negotiation

You (or lawyer) negotiate for higher compensation

Step 6: Final Settlement

Once agreed:

- You sign release

- Receive payment

Biggest Mistakes That Reduce Your Settlement

❌ Accepting first offer

❌ Not hiring a lawyer

❌ Delaying medical treatment

❌ Posting on social media

❌ Giving recorded statement without advice

Pro Tips to Maximize Your Settlement 💡

✔ Get medical treatment immediately

✔ Keep all bills and reports

✔ Avoid talking too much to insurers

✔ Hire a car accident lawyer

✔ Never accept first offer

Pros & Cons of Insurance Settlements✅ Pros

- Faster than court trials

- Guaranteed compensation

- Less stress

- Lower legal costs

❌ Cons

- May get less than court verdict

- Insurance pressure tactics

- Requires negotiation skills

Quick Comparison: Settlement vs Lawsuit

| Feature | Settlement | Lawsuit |

|---|---|---|

| Time | Fast | Slow |

| Risk | Low | High |

| Payout | Moderate | High |

| Stress | Low | High |

Powerful Insight (Most People Miss This)

👉 Insurance companies track your behavior

If you:

- Miss doctor appointments

- Delay treatment

- Act “normal” on social media

➡️ They reduce your payout significantly

What Happens After You Accept Settlement?

Once you accept:

- You cannot reopen the case ❌

- You waive your rights

- Payment is processed (usually 2–6 weeks)

👉 So think carefully before signing

Conclusion

Car accident settlements in the USA are not just about luck — they are about strategy.

If you understand:

- How insurance companies think

- How settlements are calculated

- And how to negotiate

👉 You can turn a small offer into a life-changing payout

FAQs

1. How long does a settlement take?

Usually 2 weeks to 6 months, depending on complexity.

2. Can I settle without a lawyer?

Yes, but you may get much lower compensation.

3. Is settlement taxable?

Generally not taxable, except certain damages.

4. What if insurance denies my claim?

You can appeal or file a lawsuit.

5. How much do lawyers charge?

Usually 33%–40% contingency fee.

6. Can I reopen a settlement?

No — once signed, it’s final.

7. What is a good settlement amount?

Depends on injury — ranges from $3,000 to millions.

8. Do all cases go to court?

No — 95% settle out of court.

9. Can I negotiate settlement myself?

Yes, but experience matters.

10. What is the first offer like?

Usually very low (lowball offer).

Advanced Strategies to Maximize Your Settlement (3X–10X Increase)

The Truth Insurance Companies Don’t Want You to Know

Let’s be brutally honest…

After an accident, insurance companies already have a plan:

- Delay your claim

- Confuse you with paperwork

- Offer a lowball settlement

- Pressure you to accept quickly

👉 Why?

Because most people don’t know how to negotiate

But here’s the powerful shift:

The moment you understand their strategy… you flip the game.

🔥 The “3X–10X Settlement Rule”

There’s a hidden pattern in most cases:

| Scenario | Settlement |

|---|---|

| No strategy | $5,000 – $10,000 |

| Basic negotiation | $15,000 – $40,000 |

| Expert strategy (lawyer-level) | $50,000 – $250,000+ |

👉 Same accident. Different approach. Massive difference.

Step-by-Step Strategy to Increase Your Settlement

1. Never Accept the First Offer ❌

This is the biggest mistake people make.

👉 First offers are intentionally LOW.

Example:

- Insurance offer: $12,000

- Actual case value: $60,000

What to do instead:

✔ Always respond with a counteroffer

✔ Show evidence

✔ Stay patient

Rule: If they offered it easily… it’s too low.

2. Build a “High-Value Case File”

Think of your case like a product you’re selling.

👉 The better the “proof”, the higher the price.

Your Case File Must Include:

✔ Medical reports

✔ Doctor prescriptions

✔ Bills & receipts

✔ Accident photos/videos

✔ Police report

✔ Witness statements

Pro Tip 💡

Create a timeline document:

- Day 1: Accident

- Day 3: Pain increased

- Day 10: MRI scan

- Day 30: Therapy

👉 This shows seriousness → increases payout

3. Use the “Pain Multiplier Hack” 💰

Insurance companies calculate:

👉 Medical Bills × Multiplier (1.5 to 5)

How to Increase Multiplier:

| Action | Effect |

|---|---|

| Regular doctor visits | Increases credibility |

| Specialist treatment | Higher multiplier |

| Physical therapy | Long-term impact proof |

| Mental health therapy | Adds emotional damages |

Example:

- Bills: $15,000

- Multiplier: 2 → $30,000 ❌

- Multiplier: 4 → $60,000 ✅

👉 Same bills. Double payout.

4. Don’t Talk Too Much to Insurance Adjusters 🤫

They are trained professionals.

Their goal:

👉 Make you say something that reduces your claim

What NOT to say:

❌ “I’m feeling better now”

❌ “It was partly my fault”

❌ “It’s not a big injury”

What to say instead:

✔ “I’m still under medical evaluation”

✔ “I’ll provide documents through my representative”

5. Social Media Can Destroy Your Claim 📱

Yes… even a single post can ruin everything.

Example:

You post:

👉 Gym selfie 💪

Insurance argument:

👉 “He is not injured — reduce payout”

Rule:

🚫 No posting about:

- Travel

- Gym

- Activities

- “Happy life” updates

Until case is closed.

6. Hire a Car Accident Lawyer (Game Changer)

Here’s the truth:

👉 Insurance companies take you seriously ONLY when a lawyer is involved.

Why lawyers increase payouts:

✔ Know legal loopholes

✔ Handle negotiations

✔ Calculate true claim value

✔ Threaten lawsuits (big leverage)

Real Impact:

| Without Lawyer | With Lawyer |

|---|---|

| $10,000 | $50,000+ |

| Low negotiation | Aggressive negotiation |

| High risk | Professional handling |

But what about fees?

👉 Most work on contingency basis

Meaning:

- No upfront payment

- Paid only if you win

7. Use “Delay Strategy” to Your Advantage ⏳

Insurance companies delay to frustrate you…

👉 But you can reverse it.

Smart Move:

- Don’t rush settlement

- Wait until treatment is complete

- Show long-term impact

👉 The longer (strategically) → the higher the value

8. Demand Letter Strategy (Secret Weapon)

This is what lawyers use to get BIG settlements.

What is a Demand Letter?

A document that includes:

- Full injury details

- Total damages

- Emotional impact

- Exact compensation demand

Example Structure:

- Accident summary

- Liability proof

- Medical treatment

- Financial losses

- Pain & suffering

- Final demand amount

👉 A strong demand letter can double your settlement

9. Understand Insurance Policy Limits

Even if your case is strong…

👉 You may hit a policy limit wall

Example:

- Case value: $300,000

- Insurance limit: $100,000

👉 You may only get $100,000 (unless you sue personally)

Pro Strategy:

✔ Check:

- At-fault driver’s policy

- Your own coverage (UM/UIM insurance)

10. Use “Emotional Damage Proof” 🧠

This is where most people lose money…

You can claim for:

✔ Anxiety

✔ PTSD

✔ Sleep issues

✔ Depression

How to prove it:

- Therapy sessions

- Psychologist reports

- Personal journal

👉 This can add $10,000–$100,000+ extra

Advanced Negotiation Script (Use This)

When insurance gives low offer:

👉 Say this:

“Based on my medical records, ongoing treatment, and documented pain and suffering, your offer does not reflect the true value of my claim. I am prepared to pursue further legal action if necessary.”

🔥 This line creates pressure.

Biggest Settlement Boosters 🚀

✔ Strong medical evidence

✔ Long-term injury proof

✔ Lawyer involvement

✔ High-quality demand letter

✔ Patience in negotiation

Common Tricks Insurance Companies Use

⚠️ Be aware:

- Delay tactics

- Blaming you partially

- Asking for recorded statements

- Quick settlement pressure

- Monitoring your activity

Case Study: From $9,000 to $120,000

Sarah (Texas)

- Initial offer: $9,000

- Hired lawyer

- Documented therapy + mental stress

👉 Final settlement: $120,000

Pros & Cons of Hiring a Lawyer

✅ Pros

- Higher settlement

- Less stress

- Professional handling

- Better negotiation

❌ Cons

- 30–40% fee

- Less control

Quick Checklist Before You Settle

✔ All treatments completed

✔ All bills collected

✔ Future costs estimated

✔ Emotional damages included

✔ Lawyer consulted

1. Can I negotiate without a lawyer?

Yes, but results are usually lower.

2. How much should I counteroffer?

Usually 2x–3x initial offer.

3. What if insurance refuses to increase?

Threaten legal action or hire a lawyer.

4. Is delay good or bad?

Strategic delay = good.

5. Can emotional stress increase payout?

Yes, significantly.

6. Should I record calls?

Depends on state laws.

7. What is a demand letter?

A formal compensation request document.

8. Can I switch lawyers?

Yes, anytime.

9. What if I was partially at fault?

Your payout will be reduced.

10. Do all lawyers give free consultation?

Most do.

Laws, State Rules & Legal Secrets That Decide Your Settlement

Why Law Knowledge = More Money 💰

Most people lose thousands (even lakhs in INR value) simply because they don’t understand legal rules.

Here’s the truth:

Two people with the same injury can get completely different settlements — just because of state laws.

In the USA, each state has different rules that directly affect:

- Your compensation

- Your eligibility

- Your negotiation power

Let’s break it down in a simple, practical way.

1. Fault vs No-Fault States (Game-Changing Rule)

This is the #1 legal factor that decides your settlement.

🔴 Fault-Based States (Most Common)

In these states:

👉 The person who caused the accident pays

✔ You can:

- File claim against other driver

- Sue for full damages

- Claim pain & suffering

🟢 No-Fault States

In these states:

👉 Your own insurance pays first

✔ You can:

- Use Personal Injury Protection (PIP)

- Only sue in serious injury cases

No-Fault States List

- Florida

- New York

- Michigan

- New Jersey

- Pennsylvania (choice system)

- Hawaii

- Massachusetts

- Minnesota

- Utah

- North Dakota

Key Insight 💡

👉 In no-fault states, settlements are usually:

- Faster

- But sometimes lower

👉 In fault states, settlements can be:

- Higher

- But take longer

2. Comparative Negligence Rule (Hidden Money Killer)

This rule decides:

👉 “How much fault is yours?”

Types of Comparative Negligence

1. Pure Comparative Negligence

Even if you are 99% at fault, you can still claim 1%

✔ Example:

- Total damage: $100,000

- Your fault: 70%

👉 You get: $30,000

2. Modified Comparative Negligence (Most Common)

👉 You only get compensation if fault is below 50% or 51%

✔ Example:

- Fault: 40% → You get 60% payout

- Fault: 55% → You get nothing ❌

States Using Modified Rule

- Texas

- California

- Georgia

- Illinois

3. Contributory Negligence (Strict Rule)

👉 Even 1% fault = ZERO compensation

States:

- Alabama

- Maryland

- Virginia

- North Carolina

🚨 Pro Tip

Insurance companies try to:

👉 Increase your fault percentage

Because:

➡️ More fault = Less payout

3. Statute of Limitations (Deadline That Can Kill Your Case)

This is VERY important ⚠️

👉 It defines how long you have to file a claim.

General Rule:

| Case Type | Time Limit |

|---|---|

| Personal Injury | 1–3 years |

| Property Damage | 2–6 years |

Examples:

- California → 2 years

- Texas → 2 years

- New York → 3 years

- Florida → 2 years

🚨 Warning

If you miss the deadline:

👉 Your case is PERMANENTLY CLOSED

No negotiation. No settlement. Nothing.

4. When Should You File a Lawsuit Instead of Settling?

Most cases settle…

But sometimes, lawsuit = bigger money

File Lawsuit When:

✔ Insurance denies claim

✔ Offer is too low

✔ Serious injury involved

✔ Liability is disputed

✔ Long-term damage exists

Settlement vs Lawsuit (Deep Comparison)

| Factor | Settlement | Lawsuit |

|---|---|---|

| Time | Fast | 1–3 years |

| Risk | Low | High |

| Stress | Low | High |

| Compensation | Medium | Very High |

| Control | Less | More |

Hidden Truth 🔥

👉 Just filing a lawsuit often forces insurance to:

➡️ Increase their offer quickly

5. High-Paying States for Car Accident Settlements 💰

Some states give higher payouts due to laws and jury trends.

Top High Settlement States:

- California

- New York

- Florida

- Texas

- Illinois

Why these states pay more:

✔ Higher medical costs

✔ Larger jury awards

✔ Strong legal system

✔ More aggressive lawyers

6. Insurance Policy Types That Affect Settlement

Most people don’t even know this…

👉 Different policies = different payout potential

1. Liability Insurance

Covers:

- Damage to others

👉 This is what you claim from at-fault driver

2. Personal Injury Protection (PIP)

Covers:

- Your own medical expenses

👉 Common in no-fault states

3. Uninsured / Underinsured Motorist (UM/UIM)

👉 VERY IMPORTANT

If other driver:

- Has no insurance

- Has low coverage

✔ Your own policy pays

💡 Pro Tip

Always check:

- Your UM/UIM coverage

👉 This can unlock extra compensation

7. Medical Documentation Laws (Underrated Factor)

Without proper documentation:

👉 Your case becomes weak

You MUST have:

✔ Doctor diagnosis

✔ Treatment plan

✔ Prescription records

✔ Follow-up visits

Gap in Treatment = Danger ❌

If you delay treatment:

👉 Insurance says:

➡️ “Injury is not serious”

8. Recorded Statements — Legal Trap 🎤

Insurance may ask:

👉 “Can we record your statement?”

Truth:

This is used against you.

You should:

✔ Politely refuse

✔ Speak through lawyer

9. Settlement Release Form (Final Legal Step)

Before payment, you sign:

👉 Release Agreement

What it means:

✔ Case is closed forever

✔ No future claims allowed

✔ You accept final amount

⚠️ Warning

Never sign without:

- Reviewing carefully

- Consulting a lawyer

10. Real Case Breakdown (Legal Impact Example)

Case: Mike (New York)

- Injury: Back damage

- Initial offer: $20,000

What changed?

✔ Filed lawsuit

✔ Strong medical records

✔ State law advantage

👉 Final settlement: $180,000

Biggest Legal Mistakes That Destroy Settlements

❌ Missing deadline

❌ Admitting fault

❌ No medical proof

❌ Accepting low offer

❌ Not understanding state laws

Pro Legal Hacks Used by Experts 🧠

✔ File claim early but settle late

✔ Increase medical documentation

✔ Use legal pressure (lawsuit threat)

✔ Avoid recorded statements

✔ Build emotional damage proof

Quick Legal Checklist ✅

✔ Know your state law

✔ Track limitation deadline

✔ Calculate fault percentage

✔ Verify insurance policies

✔ Consult lawyer before settlement

Conclusion

Understanding legal rules is like unlocking a hidden cheat code in car accident settlements.

If you know:

- Fault laws

- Deadlines

- Insurance structures

👉 You instantly gain power in negotiation

Because in the USA:

The person who understands the law… wins the money.

FAQs

1. What is comparative negligence?

It reduces your payout based on your fault percentage.

2. What happens if I miss deadline?

You lose your case completely.

3. Can I sue after settlement?

No.

4. What is no-fault insurance?

Your insurance pays first.

5. Which states give highest payouts?

California, New York, Florida.

6. Should I always file lawsuit?

Only if settlement is unfair.

7. What is UM/UIM coverage?

Protection against uninsured drivers.

8. Can I claim emotional damages?

Yes.

9. Do all states have same laws?

No.

10. Is lawyer necessary?

Highly recommended.

Complete Claim Blueprint + Templates + MAX Payout Strategy

Final Stage: Turning Your Claim Into Maximum Money 💰

Now you’ve learned:

- How settlements work

- How to negotiate

- How laws affect payouts

👉 This final part gives you execution power

Because knowledge alone doesn’t pay…

Execution does.

This section is your step-by-step blueprint to go from accident → claim → maximum settlement payout

🔥 Step-by-Step Car Accident Claim Blueprint (USA)

Step 1: Immediately After the Accident

Your actions in the first 24 hours can decide your entire settlement.

Do This Immediately:

✔ Call police

✔ Take photos/videos

✔ Collect driver details

✔ Get witness contact

✔ Seek medical attention

🚨 Pro Tip

Even if you feel fine…

👉 Always visit a doctor

Some injuries appear after 24–72 hours

(whiplash, internal injury, brain trauma)

Step 2: Notify Insurance Company

You must inform:

- Your insurance

- Other driver’s insurance

What to say:

✔ Basic facts only

✔ No assumptions

✔ No admission of fault

What NOT to say:

❌ “It was my mistake”

❌ “I’m okay”

❌ “No need for medical help”

Step 3: Start Medical Treatment (Critical Phase)

This is the foundation of your settlement value

Follow This Rule:

👉 No gaps in treatment

Maintain Records:

✔ Hospital bills

✔ Prescriptions

✔ Reports (X-ray, MRI)

✔ Therapy sessions

💡 Pro Insight

More consistent treatment = higher payout

(Not fake — but properly documented)

Step 4: Calculate Your Claim Value

Before negotiating, know your worth.

Your claim includes:

| Damage Type | Examples |

|---|---|

| Economic | Medical bills, lost income |

| Non-economic | Pain, suffering, trauma |

| Future damages | Long-term treatment |

Rough Calculation Formula:

👉 (Medical Bills × Multiplier) + Lost Income + Future Costs

Example:

- Medical: $20,000

- Multiplier: 3 → $60,000

- Lost income: $10,000

👉 Total claim: $70,000

Step 5: Prepare a Powerful Demand Letter

This is your money-making document

📄 Demand Letter Template (Use This)

Subject: Car Accident Settlement Demand

Dear [Insurance Company Name],

I am writing regarding the accident that occurred on [Date].

The insured party was clearly at fault, as supported by the police report and evidence.

As a result of the accident, I suffered:

- Physical injuries requiring medical treatment

- Financial losses including medical expenses and lost wages

- Emotional distress and ongoing pain

My total damages are as follows:

- Medical expenses: $_____

- Lost wages: $_____

- Pain and suffering: $_____

Based on the above, I demand a settlement amount of $_____.

If a fair settlement is not reached, I am prepared to pursue legal action.

Sincerely,

[Your Name]

🔥 Pro Tip

👉 Always demand higher than expected settlement

Because:

➡️ Negotiation will bring it down

Step 6: Negotiation Strategy (Real Game)

Now comes the battle phase

Golden Rules:

✔ Never accept first offer

✔ Stay calm and professional

✔ Use evidence as weapon

✔ Increase pressure gradually

Negotiation Flow:

- Insurance offers low amount

- You reject politely

- Provide counteroffer

- Show strong documentation

- Mention legal action possibility

Step 7: When to Bring in a Lawyer

You should hire a lawyer if:

✔ Settlement offer is too low

✔ Injury is serious

✔ Fault is disputed

✔ Claim is denied

Expected Impact:

👉 Settlement can increase 2X–5X

Step 8: Final Settlement & Payment

Once you agree:

✔ Sign release form

✔ Case is closed

✔ Payment processed (2–6 weeks)

⚠️ Final Warning

After signing:

👉 You can NEVER claim again

🚀 Advanced MAX Payout Strategy

1. Stack Multiple Claims

You can claim from:

✔ At-fault driver insurance

✔ Your own insurance

✔ UM/UIM coverage

👉 This increases total payout significantly

2. Document “Life Impact”

Don’t just show bills…

👉 Show how life changed:

- Can’t work properly

- Sleep problems

- Family impact

- Mental stress

3. Use Expert Reports

✔ Doctors

✔ Therapists

✔ Accident reconstruction experts

👉 Adds credibility → higher settlement

4. Leverage Lawsuit Threat

You don’t always need to file…

👉 Just showing readiness increases offer

5. Time Your Settlement Smartly

❌ Don’t settle early

✔ Wait until full recovery known

💰 Real High-Payout Scenario

David (Florida)

- Initial offer: $15,000

- Used full strategy

- Hired lawyer

- Built emotional damage proof

👉 Final settlement: $210,000

📊 Complete Settlement Strategy Summary

| Step | Action | Impact |

|---|---|---|

| 1 | Immediate evidence | Strong case |

| 2 | Medical treatment | Higher value |

| 3 | Documentation | Proof |

| 4 | Demand letter | Negotiation power |

| 5 | Lawyer | Huge boost |

| 6 | Patience | Max payout |

🏁 Final Conclusion

If you follow this complete blueprint:

✔ Avoid common mistakes

✔ Build strong evidence

✔ Negotiate like a pro

✔ Use legal strategies

👉 You can turn your accident into a maximum financial recovery

❓ FAQs

1. What is the fastest way to settle?

Accept first offer (not recommended).

2. What is the smartest way?

Negotiate + wait + document properly.

3. Can I get settlement without injury?

Yes, for property damage.

4. How much should I demand?

2x–3x expected amount.

5. Can I settle without court?

Yes, most cases do.

6. What increases settlement most?

Medical proof + lawyer.

7. Can I claim mental stress?

Yes.

8. Is settlement guaranteed?

No.

9. What if other driver has no insurance?

Use UM/UIM coverage.

10. How long does full process take?

Few weeks to 1 year.