Credit Card Interest Calculator (2026 Guide) :The Most Expensive Mistake Credit Card Users Make

Most people think:

👉 “I’ll just pay the minimum due… it’s fine.”

But here’s the reality:

- Interest keeps compounding

- Your debt barely reduces

- You end up paying 2x–3x more than you borrowed

👉 And the worst part?

Most people don’t even realize how much interest they’re actually paying

That’s where a Credit Card Interest Calculator becomes powerful.

💡 What a Credit Card Interest Calculator Does

A Credit Card Interest Calculator helps you:

- Calculate total interest paid

- See how long repayment will take

- Understand minimum payment trap

- Plan faster payoff strategy

👉 It shows you the real cost of your debt

🔗 Use Your Calculator

👉 https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/loan-interest-calculator/

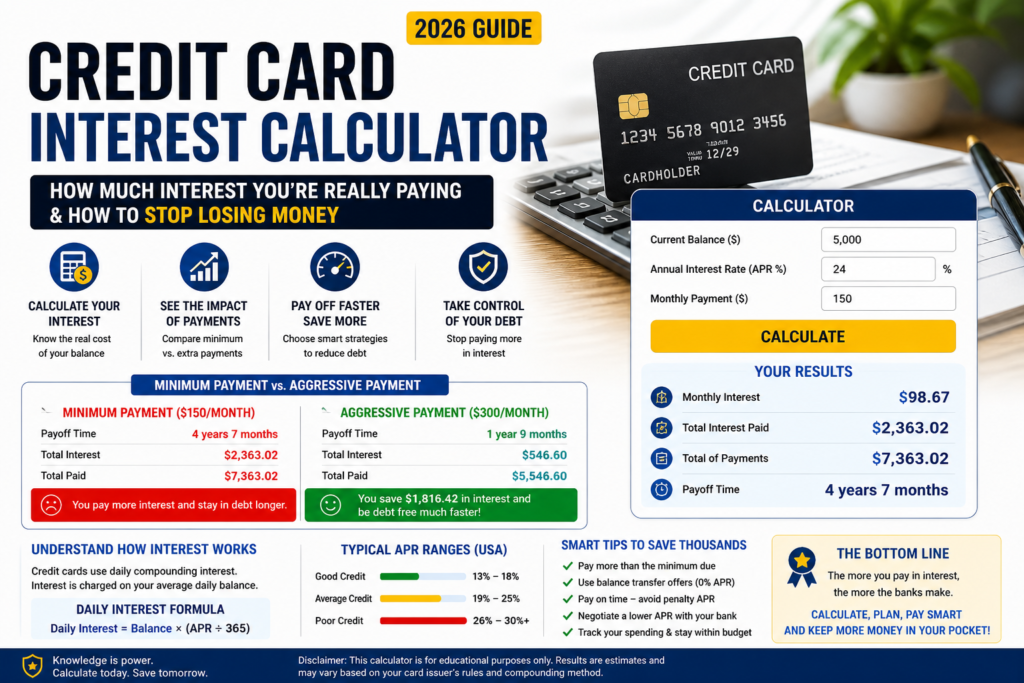

📖 Real Story: How $5,000 Debt Turned Into $11,200

Jason (name changed) had:

- Credit card debt: $5,000

- Interest rate: 24% APR

- Minimum payment: $150/month

💰 What He Thought

👉 “I’ll pay minimum… debt will go down slowly.”

⚠️ Reality

After using a calculator:

- Total repayment time: 5+ years

- Total paid: $11,200

👉 Interest alone: $6,200

💥 The Wake-Up Call

Jason realized:

👉 He was paying more in interest than the original debt

⚖️ What He Did

- Increased monthly payment

- Used structured payoff plan

- Reduced interest burden

🔥 Lesson

👉 Minimum payment = maximum interest

How to Calculate Interest, Avoid Hidden Charges & Pay Off Debt Faster 💳

If you’re carrying a balance on your credit card, here’s the uncomfortable truth:

👉 Interest is designed to keep you in debt longer.

But once you understand how it’s calculated, you can flip the game—and save thousands.

This guide shows you exact formulas, real examples, and smart payoff strategies (USA-focused).

💰 1. What Is a Credit Card Interest Calculator?

A Credit Card Interest Calculator helps you:

✔️ Estimate how much interest you’ll pay

✔️ See how long it takes to clear your debt

✔️ Compare minimum vs aggressive payments

🧮 2. Core Formula: How Credit Card Interest Works

Unlike simple loans, credit cards use daily compounding interest.

👉 Basic Formula:

Interest = Balance × Daily Rate × Number of Days

Where:

- APR (Annual Percentage Rate) = 18%–30% (typical in the USA)

- Daily Rate = APR ÷ 365

🎯 Example:

- Balance = $5,000

- APR = 24%

👉 Daily rate = 0.24 ÷ 365 = 0.000657

👉 Daily interest = $5,000 × 0.000657 = $3.29

👉 Monthly interest ≈ $98.7

⚠️ 3. The Minimum Payment Trap (Biggest Mistake)

Most Americans fall into this trap:

👉 Paying only minimum due

📉 Example:

- Balance = $5,000

- APR = 24%

- Minimum payment = $150

👉 Time to pay off = 4+ years

👉 Total interest paid = $2,000+

🔥 Reality:

Banks love minimum payments because:

✔️ You pay more interest

✔️ Debt lasts longer

📊 4. Real Interest Cost Breakdown

| Balance | APR | Monthly Interest |

|---|---|---|

| $1,000 | 20% | ~$16 |

| $5,000 | 24% | ~$100 |

| $10,000 | 26% | ~$217 |

👉 Higher balance + higher APR = explosive interest growth

💡 5. Advanced Calculation (Used by Experts)

👉 Compound Interest Formula:

Interest is added daily, so real cost is higher than simple math.

👉 Approx formula:

Final Balance = Principal × (1 + Daily Rate)^(Days)

🎯 Example:

- $5,000 at 24% APR for 1 year

👉 Final balance ≈ $6,360+

✔️ That’s $1,360 interest without aggressive payments

💳 6. Types of Credit Card Interest You Must Know

1. Purchase APR

👉 Regular spending interest

2. Cash Advance APR

👉 Higher (often 25%–35%)

3. Penalty APR

👉 Triggered after missed payments

🚀 7. How to Reduce Credit Card Interest FAST

🔥 Strategy 1: Pay More Than Minimum

Even +$50/month can save thousands

🔁 Strategy 2: Balance Transfer (0% APR Cards)

👉 Transfer debt to 0% intro APR card (12–21 months)

✔️ Pay principal without interest

💣 Strategy 3: Debt Avalanche Method

- Pay highest APR first

- Minimum on others

👉 Saves maximum interest

❄️ Strategy 4: Debt Snowball Method

- Pay smallest balance first

- Builds motivation

📉 Strategy 5: Negotiate Lower APR

Call your bank:

👉 Ask for APR reduction

✔️ Works surprisingly often

🧠 8. Credit Card Interest vs Other Debt

| Type | Interest Rate | Risk |

|---|---|---|

| Credit Card | 18%–30% | Very high |

| Personal Loan | 10%–18% | Medium |

| Mortgage | 5%–8% | Low |

👉 Credit cards = most expensive debt

⚡ 9. Smart Payoff Strategy (2026)

Step-by-Step:

- List all cards

- Identify highest APR

- Pay aggressively

- Use balance transfer if possible

- Avoid new spending

📊 10. Real-Life Scenario

🎯 Case:

- Total credit card debt: $8,000

- APR: 22%

❌ Minimum payment route:

- Payoff time: 5 years

- Interest paid: $3,500+

✅ Aggressive payoff ($400/month):

- Payoff time: ~2 years

- Interest paid: ~$1,800

👉 Savings = $1,700+

🛠️ 11. Build Your Own Credit Card Interest Calculator

Inputs:

- Balance

- APR

- Monthly payment

Outputs:

- Monthly interest

- Total interest

- Payoff time

⚙️ How Credit Card Interest Is Calculated

Step 1: APR (Annual Percentage Rate)

👉 Example: 24% APR

Step 2: Daily Interest Rate

👉 Formula:

APR ÷ 365

👉 Example:

24% ÷ 365 = 0.065% per day

Step 3: Daily Compounding

Interest is added daily on your balance.

Step 4: Monthly Billing

Total interest added to your bill.

🧮 Simple Formula

👉 Interest = Balance × (APR ÷ 365 × Days)

📊 Real Interest Examples

| Balance | APR | Time | Interest Paid |

|---|---|---|---|

| $2,000 | 20% | 2 yrs | ~$800 |

| $5,000 | 24% | 5 yrs | ~$6,200 |

| $10,000 | 25% | 7 yrs | ~$15,000 |

🔥 Why Credit Card Interest Is So Dangerous

1. High APR

20%–30% is common

2. Daily Compounding

Interest grows every day

3. Minimum Payment Trap

Keeps you stuck for years

4. Psychological Comfort

“Minimum due” feels safe

👉 But it’s not.

🔗 Internal Tools (Smart Financial System)

👉 Debt Settlement Calculator

https://claimjusticeusa.com/debt-credit-settlement-calculator/

👉 Financial Health Score

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/financial-health-score-calculator/

👉 Budget Calculator

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/budget-calculator/

👉 Credit Score Simulator

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/credit-score-simulator/

🧠 Advanced Insight: Why Banks Love Minimum Payments

Banks earn from:

- Interest, not principal

👉 Minimum payment ensures:

- Longer repayment

- Higher profit

💬 How to Reduce Credit Card Interest (Pro Strategies)

✔ Pay More Than Minimum

Even +$50 saves thousands

✔ Use Snowball Method

Pay smallest debt first

✔ Use Avalanche Method

Pay highest interest first

✔ Balance Transfer

Shift to lower interest card

✔ Debt Settlement (If Needed)

Reduce total amount

⚠️ Mistakes That Increase Interest

- Paying only minimum

- Missing payments

- Using multiple cards

- Ignoring APR

⏱ Payoff Comparison

| Strategy | Time | Interest |

|---|---|---|

| Minimum payment | 5–10 years | High |

| Double payment | 2–4 years | Medium |

| Aggressive payoff | <2 years | Low |

💸 Credit Card Interest vs Loan Interest

| Type | Interest Rate |

|---|---|

| Credit Card | 20%–30% |

| Personal Loan | 10%–18% |

| Home Loan | 6%–10% |

👉 Credit cards are the most expensive debt

🌐 External Sources

👉 https://www.consumerfinance.gov

👉 https://www.investopedia.com

❓ FAQs

- How is credit card interest calculated?

👉 Daily compounding - What is APR?

👉 Annual interest rate - Why is interest so high?

👉 Unsecured lending - What is minimum payment trap?

👉 Paying mostly interest - How to reduce interest?

👉 Pay more - Can I avoid interest?

👉 Pay full balance - What is grace period?

👉 Interest-free time - What happens if I miss payment?

👉 Penalty + higher APR - Is calculator accurate?

👉 Yes (estimate) - How much interest is normal?

👉 20%–30% - Can I negotiate interest?

👉 Sometimes - What is balance transfer?

👉 Moving debt - Can I settle credit card debt?

👉 Yes - What is compound interest?

👉 Interest on interest - Does interest affect credit score?

👉 Indirectly - What is best repayment method?

👉 Avalanche - Can I reduce APR?

👉 Yes (negotiation) - What is revolving credit?

👉 Ongoing balance - Is credit card debt bad?

👉 High-risk - How to become debt-free fast?

👉 Aggressive payments

🧾 Conclusion

Credit card interest is not just a fee…

👉 It’s a system designed to keep you paying longer.

But once you understand it:

👉 You can break free.

🔥 Final Thought

Banks make money when you stay in debt.

👉 You win when you understand the numbers.

Calculate smart. Pay smart. Get free faster.

⚠️ Disclaimer

This content is for informational purposes only and not financial advice.