Debt & Credit Settlement Calculator (2026 Guide): The Silent Financial Trap Most People Fall Into

Debt doesn’t destroy you overnight.

It builds slowly:

- One credit card

- One missed payment

- One emergency

And then suddenly…

👉 You’re paying interest, not your actual debt

That’s when most people think:

👉 “I’ll just pay minimum dues and manage it.”

But here’s the harsh truth:

👉 Minimum payments keep you trapped for years

That’s where debt settlement becomes powerful.

💡 What a Debt & Credit Settlement Calculator Actually Does

A Debt Settlement Calculator shows you:

- How much debt you can reduce

- How much you’ll actually pay

- How long settlement will take

- How much you save

👉 It gives you a clear exit strategy

🔗 Start With Your Calculator

👉 https://claimjusticeusa.com/debt-credit-settlement-calculator/

How Much You Can Save, How Negotiations Work & How to Eliminate Debt Fast 💳

If you’re buried in credit card bills, personal loans, or collections, here’s the truth:

👉 You don’t always have to pay 100% of your debt.

With the right strategy, people regularly settle debts for 30%–70% less than what they owe.

This guide breaks down exact calculation methods, real examples, and smart strategies so you can estimate—and maximize—your savings.

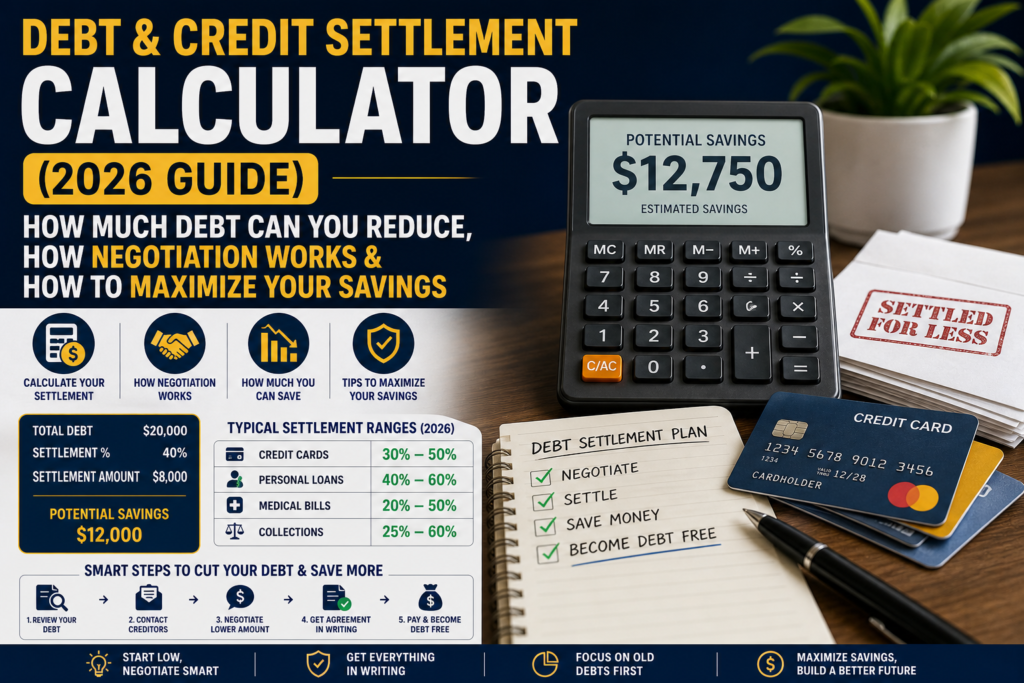

💰 1. What Is a Debt Settlement Calculator?

A Debt Settlement Calculator estimates:

✔️ How much you actually need to pay

✔️ How much you can save

✔️ How long it will take to become debt-free

It works by applying negotiation ranges + financial ratios used by banks, collectors, and settlement agencies.

🧮 2. Core Formula: How Debt Settlement Is Calculated

👉 Basic Formula:

Settlement Amount = Total Debt × Settlement Percentage

🎯 Example:

- Total debt = $20,000

- Settlement percentage = 40%

👉 You pay = $8,000

👉 You save = $12,000

📊 3. Realistic Settlement Percentage Ranges (2026)

| Debt Type | Typical Settlement |

|---|---|

| Credit Cards | 30% – 50% |

| Personal Loans | 40% – 60% |

| Medical Bills | 20% – 50% |

| Collections | 25% – 60% |

👉 Older debts = higher discount

👉 Recently defaulted debt = lower discount

⚖️ 4. How Creditors Actually Decide Your Settlement

Banks don’t randomly pick numbers. They evaluate risk vs recovery.

🔍 Key Factors That Affect Your Settlement:

1. Payment History

- Missed payments = higher chance of settlement

- Current accounts = low negotiation power

2. Financial Hardship

If you can prove:

- Job loss

- Medical emergency

- Business failure

👉 You unlock better deals

3. Debt Age (VERY IMPORTANT)

| Age of Debt | Impact |

|---|---|

| 0–3 months | Low settlement chance |

| 6–12 months | Moderate |

| 12+ months | High settlement |

4. Lump Sum vs EMI Settlement

- Lump sum = maximum discount

- Installments = smaller discount

💸 5. Advanced Calculation Model (Used by Experts)

Professionals don’t just use percentages—they calculate:

👉 Net Settlement Cost Formula:

Total Cost = Settlement Amount + Fees + Taxes

Example:

- Debt: $20,000

- Settlement: $8,000

- Company fee (20%): $1,600

👉 Total cost = $9,600

✔️ Still saving: $10,400

🏦 6. DIY vs Debt Settlement Company (Which Is Better?)

🔥 Option 1: Do It Yourself (DIY)

Pros:

- No fees

- Full control

Cons:

- Hard negotiation

- Time-consuming

🚀 Option 2: Settlement Company

Pros:

- Professional negotiation

- Faster results

Cons:

- 15%–25% fees

👉 Smart strategy:

Start DIY → If stuck → hire expert

📉 7. How Debt Settlement Affects Your Credit Score

This is where most people make mistakes.

⚠️ Reality:

- Credit score can drop 100–150 points

- Settled accounts show as: “Settled” not “Paid in Full”

📈 But Here’s the Recovery Timeline:

| Time | Impact |

|---|---|

| 0–3 months | Score drops |

| 3–6 months | Stabilizes |

| 6–12 months | Starts improving |

| 12–24 months | Strong recovery |

👉 If you’re already in default, impact is smaller.

🔥 8. Smart Strategy to Maximize Your Savings

💡 Insider Tips:

1. Always Start Low

Offer 25%–30% first

👉 Negotiate upward slowly

2. Use Silence as a Weapon

Collectors follow scripts—you don’t have to

3. Ask for “Pay for Delete”

👉 Remove negative entry from credit report

4. Target Old Debts First

👉 Highest discount potential

5. Always Get Written Agreement

Never pay without proof

🚀 9. Real-Life Case Study

🎯 Scenario:

- Total debt: $15,000

- Negotiated at 35%

👉 Paid: $5,250

👉 Saved: $9,750

✔️ Debt-free in 5 months

📊 10. Debt Settlement vs Other Options

| Option | Best For | Risk |

|---|---|---|

| Settlement | High debt, low income | Credit drop |

| Consolidation | Stable income | Interest cost |

| Bankruptcy | Extreme cases | Long-term damage |

🧠 11. When You SHOULD Use Debt Settlement

✔️ You can’t repay full debt

✔️ You’re already missing payments

✔️ Credit score is already low

❌ When You SHOULD NOT Use It

❌ You have a good credit score

❌ You can repay via EMI

❌ You need loans soon

💡 12. Hidden Costs Most People Ignore

- Settlement company fees

- Tax on forgiven debt (in some countries)

- Legal risk if creditor sues

👉 Always calculate true cost before deciding

🛠️ 13. Build Your Own Debt Settlement Calculator

You can easily create one for your website using:

Inputs:

- Total debt

- Settlement %

- Fees %

Output:

- Payable amount

- Savings

- Net cost

1. Can I settle debt for 10%?

Rare, but possible for very old debt.

2. How long does settlement take?

3–36 months depending on strategy.

3. Will I go to jail for unpaid debt?

No (civil matter in most countries).

4. Can banks refuse settlement?

Yes—but they usually negotiate.

5. Is settlement better than bankruptcy?

In most moderate cases, yes.

6. Does settlement remove interest?

Usually yes (negotiable).

7. Can I settle multiple debts?

Yes—and often recommended.

8. What is the minimum amount for settlement?

Depends on lender policy.

9. Can I settle after legal notice?

Yes—but urgency increases.

10. Does settlement affect future loans?

Yes, but temporarily.

11. Can I negotiate myself?

Absolutely—and often better.

12. Do I need a lawyer?

Not always.

13. What if creditor rejects my offer?

Counter-offer or wait.

14. Can interest keep increasing?

Yes—until settlement is finalized.

15. Is debt settlement safe?

Yes, if done properly.

Turn Debt Into a Negotiation Advantage

Most people think debt is a trap.

👉 Smart people treat it like a negotiation game.

- Start low

- Stay patient

- Negotiate aggressively

✔️ You can cut your debt by 50% or more

This guide is for educational purposes only. Laws, tax rules, and credit systems vary by country. Always consult a financial advisor or legal expert before making final decisions.

📖 Real Story: From $28,000 Debt to $11,500 Settlement

Mark (name changed) had:

- 3 credit cards

- Total debt: $28,000

- High interest (22%+)

💰 His Monthly Reality

- Minimum payment: $900

- Interest eating 70% of payment

👉 Debt wasn’t going down…

It was growing.

⚠️ The Breaking Point

After missing 2 payments, he got calls from collectors.

He thought:

👉 “I’m stuck. There’s no way out.”

🧮 The Turning Point

He used a calculator:

👉 https://claimjusticeusa.com/debt-credit-settlement-calculator/

📊 The Reality

- Original debt: $28,000

- Estimated settlement: ~$12,000

👉 Savings potential: $16,000

⚖️ What He Did Next

- Stopped minimum payments

- Negotiated settlements

- Paid lump sum in parts

💥 Final Outcome

👉 Final paid: $11,500

🔥 Lesson

👉 Debt didn’t disappear

👉 It was negotiated down

🧠 What Is Debt Settlement (Simple Explanation)

Debt settlement means:

👉 Negotiating with creditors to:

- Reduce total debt

- Pay less than owed

- Close account

Example:

- Debt: $20,000

- Settlement: $10,000

👉 You save $10,000

⚙️ How Debt Settlement Is Calculated

Step 1: Total Debt

Add all unsecured debts:

- Credit cards

- Personal loans

- Medical bills

Step 2: Settlement Percentage

👉 Typical range: 40% – 70%

Step 3: Final Payment

👉 Example:

$20,000 × 50% = $10,000

Step 4: Fees (If Using Company)

- 15% – 25% of debt

Final Formula

👉 Settlement = Total Debt × Negotiated % + Fees

📊 Real Debt Settlement Examples

| Debt Amount | Settlement | Savings |

|---|---|---|

| $10,000 | $5,000 | $5,000 |

| $25,000 | $12,500 | $12,500 |

| $50,000 | $25,000 | $25,000 |

🔥 5 Factors That Decide Your Settlement Amount

1. Amount of Debt

Higher debt = more negotiation power

2. Missed Payments

Late payments increase settlement chances

3. Creditor Policy

Some banks settle faster

4. Lump Sum Availability

Cash offer = better deal

5. Negotiation Skill

👉 Biggest factor

🔗 Internal Tools (Complete Financial Ecosystem)

👉 Loan Interest Calculator

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/loan-interest-calculator/

👉 Budget Calculator

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/budget-calculator/

👉 Financial Health Score

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/financial-health-score-calculator/

👉 Credit Score Simulator

https://claimjusticeusa.com/financial-calculator-hub/financial-calculators/credit-score-simulator/

🧠 Advanced Insight: Why Banks Agree to Settlement

Banks prefer:

- Partial recovery ✔️

- Instead of zero recovery ❌

👉 That’s why settlement works.

⚠️ Downsides of Debt Settlement

- Credit score drops

- Collection calls

- Possible legal risk

💬 Negotiation Strategy (Real Framework)

Step 1: Stop Paying Temporarily

Shows inability

Step 2: Wait for Collection Stage

Better negotiation power

Step 3: Offer Lump Sum

Start at 30%–40%

Step 4: Negotiate Upwards

Settle at 40%–60%

Step 5: Get Written Agreement

👉 Always

📉 Debt Settlement vs Other Options

| Option | Best For |

|---|---|

| Settlement | High debt |

| Consolidation | Lower interest |

| Bankruptcy | Extreme cases |

⏱ Timeline

| Stage | Time |

|---|---|

| Missed payments | 2–3 months |

| Negotiation | 3–6 months |

| Settlement | 6–12 months |

💸 Tax Rule

👉 Forgiven debt may be taxable

🌐 External Sources

👉 https://www.consumerfinance.gov

👉 https://www.ftc.gov

❓ FAQs

What is debt settlement?

👉 Paying less than total debt

- How much can I save?

👉 30%–60% - Does it hurt credit score?

👉 Yes - Is it legal?

👉 Yes - How long does it take?

👉 6–12 months - Can I negotiate myself?

👉 Yes - Do I need company?

👉 Optional - What debts qualify?

👉 Unsecured - Can I settle credit cards?

👉 Yes - What is average settlement?

👉 40%–60% - Are fees high?

👉 15%–25% - Can I stop anytime?

👉 Yes - Is it better than bankruptcy?

👉 Depends - Will creditors agree?

👉 Often yes - Can I pay in installments?

👉 Sometimes - Is forgiven debt taxable?

👉 Yes - Can legal action happen?

👉 Possible - What if I miss payments?

👉 Collection starts - Is settlement guaranteed?

👉 No - Does it clear debt fully?

👉 Yes

🧾 Conclusion

Debt settlement is not magic…

👉 It’s a strategy.

And the biggest advantage you can have is:

👉 Knowing your numbers before negotiating.

🔥 Final Thought

Banks protect their money.

👉 You should protect yours.

Calculate smart. Negotiate strong. Become debt-free.

⚠️ Disclaimer

This content is for informational purposes only and not financial advice.